Tax Compliance?

- Wilder Perez Condor

- Aug 8, 2021

- 3 min read

Updated: Aug 9, 2021

Suddenly and concerningly, the director of the government office approached my desk. I was frightened: "What happens now?", I thought. Then he asked me to help fix the mistakes on his annual tax income declaration. Before long, I was helping almost of all of my colleagues in the office after they cottoned on to my accounting skills. Now, this odd situation makes me ask myself, how come many people with less related professional specialisations have the same difficulties, but less support?

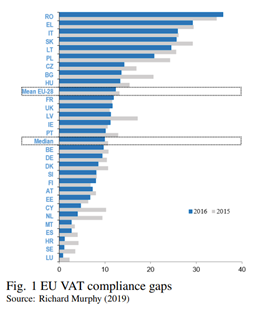

It might seem: like the Peruvian tax system is too complicated. However, it is fair to ask if these issues are common in other countries and whether the overly complicated tax declarations affect tax compliance at the national level? According to Leiceste, Level and Rasul (2012), this issue is widespread. Unsurprisingly, disparities between expected fiscal revenues and those actually received (the tax gap) varies between rich and poor countries (see Fig. 1).

To explain the lack of tax compliance, Allingham and Sandmo (1972) developed a standard model of tax compliance (percentage of people paying their taxes) based on the idea of choice under uncertainty factoring in the profitability of evading taxes and the probability of being caught. Although this theoretical approach sounds like it makes economic sense, the policy implications assume people completely understand the rules of the tax system and the consequences of disobeying them (ie they have rational expectations However, this does not hold all of the time, especially when the tax system is very complex.

Undoubtedly, a behavioural approach might be quite different from approaches using the standard model, especially when the assumption of rational expectations is relaxed

Indeed, Richarson (2006) found based on data for 45 countries, that complexity is the most relevant determinant of tax evasion, this makes the rational expectations assumption seem more problematic. In simple words, if taxpayers have bounded rationality or expectations that are not completely rational (they don’t know they system well), then the complexity of the tax system could affect compliance. People could simply make mistakes in determining their tax liabilities or the complexity could create an information asymmetry between firms and tax regulators. But it is not as simple as that. Even if a simpler tax system facilitated peoples’ tax declarations, the system’s simplicity might make tax evasion easier. In response to this, governments might add additional measures which aim to reduce evasion but also end up reintroducing the complexity.

Hence, the main purpose of this article is to open the discussion about tax compliance policies and shed some light on recent behavioural insights on this topic. Obviously, the most important thing about taxes is how you feel about contributing to your community because we know that paying taxes is not people’s favourite thing to do, as shown by the riots provoked by the subject when they were unfair. However, a friendlier and understanding but also cautious tax system could improve our coexistence.

Looking forward, the regular audits and control tax process might be affected due to the new more complex post-pandemic business cycle. Indeed, the pandemic has brought new changes such as remote working, increasing of digitisation of sales, the erosion of trust in government and the effects that has on controlling misinformation and higher demand for taxes on the wealthy. These changes also, such as the acceleration of the spread of digitisation after the COVID, may create new opportunities for governments to make the tax system easier to use.

In that sense, Behavioural Approach gives an outstanding opportunity to opens the literature to new assumptions from the traditional approach. It could also make the starting point in taxation public policies to deal with the new challenge arising from the new normal after the recent pandemic.

References

Ahmed, N., Chetty, R., Mobarak, M., Rahman, A. and Singhal, M., 2012. Improving tax compliance in developing economies. International Growth Center, Havard University.

Alm, J. and Martinez-Vazquez, J., 2007. Tax morale and tax evasion in Latin America.

Becker, G.S., 1985. Public policies, pressure groups, and dead weight costs. Journal of public economics, 28(3), pp.329-347.

Murphy, R., 2019. The European tax gap. A report for the Socialists and Democrats Group in the European Parliament. Global Policy.

Rasul, I., Tax and benefit policy: insights from behavioural economics.

Richardson, G., 2006. Determinants of tax evasion: A cross-country investigation. Journal of international Accounting, Auditing and taxation, 15(2), pp.150-169.

Comments